Chinese producers of downstream phosphorus products have recently called Force Majeure, announced large price increases or have cancelled/delayed shipments.

Aerial view of small hydroelectric station; power restrictions are causing issues for production.

1. Electricity supply problems

China’s yellow phosphorus output is concentrated in the Yunnan, Sichuan, Guizhou, and Hubei provinces’ south-western region.

Hydroelectric power generation is the main source of electricity in the south-west area and with this year’s dry period in Yunnan being longer than in previous years (December to May) generation was impacted.

It was only in May of this year that power restrictions began to escalate again in Yunnan, affecting a large proportion of the yellow phosphorus market who were forced to reduce or stagger their production.

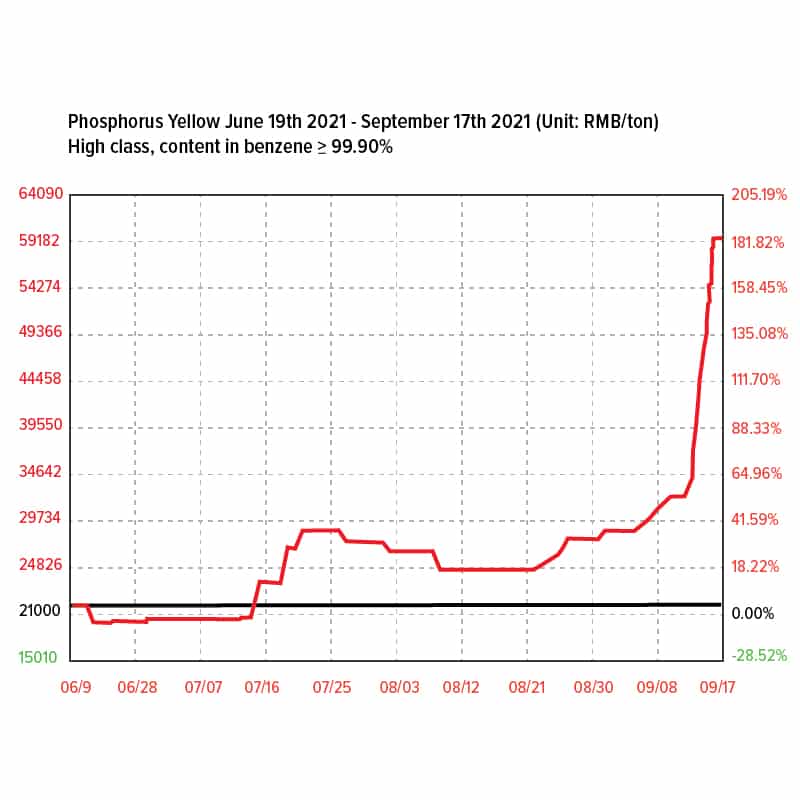

With this as a backdrop, we can see how yellow phosphorus prices began to rise noticeably from mid-May onwards and as a result the market supply tension has continued to intensify as the market essentially has not enough inventory to meet demand.

It is predicted that the price and supply of yellow phosphorus will continue to trend upwards, at least in the short term.

2. Environmental protection and production restrictions

China produced 130 million tons of phosphate ore each year until 2015, when it was at its peak.

However, environmental concerns were being raised and the potential issues that could impact the phosphate market if left unchecked for too long. Things such as uncontrolled mining and primarily small and medium-sized business practices and the impacts these have on the environment.

As a result, improving the governance and adaptation of phosphate mines has been one of China’s most significant environmental governance triumphs in recent years.

However, and as a result, under the policy of environmental protection and production restrictions China’s phosphate ore production has decreased drastically, with negative growth in production from 2016 and a negative growth rate of -27.9% in 2018.

For the first time in recent memory, production fell below 100 million tons for the first time in history and ongoing production continues to drop under the policy of environmental protection and industrial limitations.

3. Popularity of Lithium iron phosphate batteries

Power batteries are classified as being either lithium iron phosphate or ternary lithium, depending on their composition. Ternary lithium batteries have gained popularity in recent years because of their high energy density, whereas lithium iron phosphate batteries are recognized for being less expensive and safer.

The contemporary downstream application market has also increased yellow phosphorus demand this year. In 2021, the yellow phosphorus market has benefited from the surge in downstream applications. When compared to the more traditional market, the battery industry C lithium iron phosphate is a more powerful ally of the yellow phosphorus market than it was even this time last year.

As of May, the cumulative production of lithium iron phosphate was 50.3%, more than 49.6% of ternary lithium batteries, and is predicted to see year on year growth up to 80%.

Phosphorus Yellow June 19th 2021 – September 17th 2021 (Unit: RMB/ton)

Affected products

Some of the affected products that may be impacted by the issues surrounding the phosphorus market have been listed below.

Please contact your Redox representative to discuss any concerns or supply strategy.

- Soluble Fertilisers – MAP, DAP, MKP, APP

- Phosphoric Acid,

- Polyphosphoric Acid.

- Phosphorous Acid.

- Phosphonates – HEDP, ATMP, PBTC etc

- Food Grade Phosphates – SAPP etc

- Tech Grade Phosphates – STPP etc

- Glyphosate.

- Hypo phosphoric Acid.

- Sodium Hypophosphite.

- Red Phosphorous.

- Any organo phosphite/phosphate.

- Phosphine(s).