Redox proudly represents Evonik in Australia & New Zealand for their exceptional range of VISIOMER® Specialty Methacrylates.

Within the domain of macromolecular chemistry, the remarkable adaptability and efficacy of methacrylate monomers have long been acknowledged and celebrated. These versatile building blocks have solidified their indispensable status across numerous industries and applications. VISIOMER® Specialty Methacrylates have emerged as essential components, harnessing their diverse capabilities to unlock endless possibilities.

Applications & benefits

From adhesives and paints to coatings, composite resins, construction materials, and an array of unique applications, VISIOMER® Specialty Methacrylates offer individuality and sustainability, enabling exceptional effects for products across a broad spectrum.

Let us explore a selection of industries and the corresponding advantages conferred by VISIOMER® methacrylates:

Protective coatings

- Excellent weather- and scratch resistance

- SB coatings with low VOC, fast physical drying and outstanding levelling and gloss

- Excellent adhesion and corrosion resistance

Architectural Coatings

- Excellent shear stability, viscosity control and adhesion of emulsion paints to a variety of substrates

- Higher resistance against polar chemicals

- Resins with low carbon footprint

Adhesives

- Enhanced cohesive strength and resistance

- Formulation components with low hazard potential

- Increased adhesion to polar surfaces

Construction

- Fast curing, even at low temperatures

- Low-odour, reactive diluent

- Chemical stability

The remarkable potential of these specialty chemicals extends far beyond their primary applications, opening up limitless opportunities for generating unique and environmentally friendly effects across a multitude of industries, including adhesives, construction, composite resins and a whole range of specialty applications – Electrical insulation varnishes, surfactants, thickeners and 3D printing used in dental compounds, adhesives for dental applications and 3D printed aligners.

Sustainable performance

What sets the VISIOMER® line of biobased specialty methacrylate monomers apart is their exceptional ability to deliver outstanding results while prioritising sustainability. With a steadfast commitment to environmental responsibility, these methacrylates offer top-tier performance and serve as a greener alternative.

Evonik has been manufacturing monomers for over ten years using biobased and recycled raw materials, comprising up to 85% of the composition. These monomers fall under the renowned brand VISIOMER® Terra, reflecting our commitment to safeguarding the environment and addressing climate change while maintaining excellent performance standards. Not only are VISIOMER® Terra biobased monomers required to meet stringent performance criteria, but they must also possess low hazard potential and promote environmental friendliness. As their popularity continues to rise, these monomers become more affordable, ensuring wider accessibility.

How Can Redox Help?

With Redox, rest assured that our unwavering commitment to excellence will empower your business.

Contact us today to discover how we can be an essential partner in your sourcing strategy.

Ammonium chloride boasts a rich and ancient history, with its origins traced back to Ancient Egypt, where it was identified in the Temple of Zeus-Ammon. Historical records reveal that the Chinese were already harnessing the versatility of this compound as early as 554 A.D, highlighting its enduring presence throughout the ages.

How do we use it today?

In contemporary times, ammonium chloride plays a pivotal role in various industries. Ammonium chloride is a compound with the chemical formula NH₄Cl. It comprises ammonium (NH₄⁺) and chloride (Cl⁻). The ammonium ion is a positively charged polyatomic ion with the formula NH₄⁺, and the chloride ion is a negatively charged ion with the formula Cl⁻. When these ions combine, they form the ionic compound ammonium chloride. The elements involved in the formation of ammonium chloride are nitrogen (N), hydrogen (H), and chlorine (Cl).

Ammonium chloride plays a crucial part in supporting plant growth and fostering optimal soil conditions for enhanced agricultural productivity.Commercially, ammonium chloride is used as a fertiliser to supply plants with nitrogen and enhance soil structure. Some fertilisers are formulated to combine different compounds for a broader range of nutrients. Calcium-containing compounds, like calcium nitrate or calcium chloride, may be added separately to these fertilisers to improve soil structure and provide calcium as a nutrient to plants. These additional compounds are mixed with ammonium chloride or other fertilisers to create a balanced blend suitable for specific soil and plant requirements.

Surprisingly, ammonium chloride has found its way into the food industry. Beyond its use in baking to impart an exceptionally crisp texture to cookies, it serves as a flavouring agent in dark sweets like salty liquorice, particularly popular in Nordic countries, Benelux, and northern Germany. This adds an exciting and unconventional element to certain types of confectionery.

How can we help?

Redox, a global leader in ammonium chloride distribution, meets the diverse needs of customers worldwide, from Australia and New Zealand to Malaysia, the USA, and Mexico. Responding proactively to market demands, Redox remains committed to satisfying clients’ requirements globally.

Our ammonium chloride is available in various packing sizes, including 25kg and 1000kg bulk bags, coming in a range of grades such as 99.5% min powder/granular and conforming to FAMI-QS and Food Safety Regulation.

Connect with one of Redox’s experts to explore how their offerings can be integral to your sourcing strategy.

Distributed by Redox, Boric Acid is an often unsung hero in industrial chemistry and has emerged as a versatile and indispensable compound. Its utility ranges from preserving wood to influencing nuclear reactions, and its significance extends to environmental conservation.

Below, we delve into the multi-faceted world of Boric Acid, uncovering its industrial applications, pricing determinants, ecological advantages, and emerging innovations.

A Versatile Workhorse

Boric Acid, a naturally occurring compound of boron, hydrogen, and oxygen, possesses a remarkable versatility. Due to its unique properties, it has secured its place in various industries. Here are some of the notable applications:

1. Wood Preservation: Boric Acid is crucial in preserving wood, safeguarding timber against rot and decay. Its ability to prevent the growth of fungi and insects has made it a sustainable alternative to more toxic wood treatments.

2. Nuclear Energy: Boric Acid is essential for reactor cooling in the nuclear industry. It controls nuclear reactions by absorbing excess neutrons, ensuring safety and efficiency in power plants.

3. Flame Retardants: Boric Acid is a fire retardant in products like mattresses, upholstery, and textiles. It hinders combustion and slows down the spread of flames, improving safety.

4. Eyewash Solutions: In the healthcare sector, it is a crucial component of eyewash solutions used to treat eye irritation or chemical exposure.

5. Lubricants and Corrosion Inhibitors: It is employed as a lubricant additive and corrosion inhibitor, extending the life of machinery and equipment.

Pricing Factors and Market Dynamics

Cost are influenced by several factors. Primarily, the availability of boron-rich minerals, from which it is derived, plays a significant role. Global supply and demand trends, influenced by agriculture, ceramics, and electronics industries, also impact pricing. Geopolitical factors and production regulations in major producing countries, including Turkey and the United States, contribute to market volatility.

In recent years, an increase in demand, particularly from electronics and renewable energy sectors, has placed upward pressure on prices. As industries strive to reduce their environmental footprint, the demand for boric acid’s applications in sustainable practices has risen, further influencing its cost.

Growing demand for the below applications around the world has had a direct impact on the growth of the Boric Acid

- Glass

- Ceramics

- Pharmaceutical

- Pesticide

- Fertiliser

- Textile Industry

- Others

Future Market Insights recently published its findings, concluding the global boric acid market size is anticipated to increase from US$ 840.7 million in 2022 to US$ 1,409 million by 2032, exhibiting a CAGR of 5.3% during the forecast period.

Environmental Benefits and Sustainability

Boric Acid is not only prized for its industrial utility but also for its environmental advantages. Its non-toxic and low-impact properties make it an environmentally responsible choice in various applications, particularly wood preservation and flame retardants.

The chemical’s ability to enhance the longevity of products and reduce the need for toxic alternatives aligns with modern sustainability goals. As industries become more eco-conscious, Boric Acid has emerged as a green alternative to conventional, more harmful chemicals.

Innovations on the Horizon

The chemical industry, always pursuing safer, more efficient, and environmentally friendly solutions, is exploring innovative uses for Boric Acid. Researchers are investigating its potential in advanced battery technologies to improve lithium-ion batteries’ energy storage and sustainability.

Moreover, Boric Acid’s role in improving crop yields and pest resistance in agriculture is an exciting avenue for future exploration.

How Can We Help?

In the ever-evolving landscape of industrial chemistry, Boric Acid has transformed from a hidden gem to a prized asset across various industries.

Its unique properties and eco-friendly advantages make it the go-to choice as sustainability and efficiency become paramount. The journey from an industrial staple to an environmentally responsible option underscores its indispensable role in shaping a cleaner and safer world.

Redox offers Boric Acid in various specs: from 25kg film bags to 1mt bulk bags. Contact us today to explore how our Boric Acid solutions can contribute to your success.

We at Redox are excited to share that we have renewed our Chemical Educational Foundation’s Presidents Club membership. This is our way of supporting the CEF team’s efforts to promote chemistry education and raise awareness among students in grades K-8.

CEF’s You Be The Chemist programs uniquely connect business and education in local communities to reach students early in life and ignite a passion for chemistry and science-related careers.

Companies and individuals in the science and chemistry industries have invested in You Be The Chemist since 1989, to inspire young students into a lifelong passion for these fields. Programs are implemented in partnership with schools and education programs so activities align with local workforce and learning needs.

Nick Osmo, General Manager, North America, said, “I believe fostering curiosity into STEM at an early age is essential. We want our youth’s innate curiosity to overcome any intimidating aspects that otherwise might deter them so that these powerful subjects become enduring areas of interest, study and eventually a career and passion.”

In today’s world, where science, technology, engineering, and mathematics (STEM) are crucial for the future workforce, high school and post-secondary students often receive the most attention in terms of preparation.

However, it is essential to realise that igniting a passion for science at a young age, even as early as five years old, significantly enhances the likelihood of engaging students in learning and ultimately pursuing careers in STEM fields.

CEF’s outstanding program, You Be the Chemist, is dedicated to this cause. It offers educators many educational resources, including activity guides and workshops. Additionally, the program hosts an annual academic competition at the local, state, and national levels, inviting students in grades 5-8 to compete for scholarships and prizes.

The impact of CEF’s You Be the Chemist program is evident in the remarkable outcomes it has achieved.

The You Be the Chemist program continues to serve as a bridge between businesses, educational institutions, and young students, demonstrating the immense potential of chemistry to create a better world.

Epoxy resins are incredibly versatile and functional, making them essential in various industries. They are used in adhesives, coatings and are critical in many applications. Let’s quickly look into the world of epoxy resins and explore their significant impact on diverse sectors.

Epoxy resins, commonly used in various applications, are typically produced through a chemical reaction between epichlorohydrin (ECH) and bisphenol-A (BPA). This reaction results in speciality resins in either liquid or solid form. The production processes for liquid and solid epoxy resins are similar. Initially, ECH and BPA are combined in a reactor, and a solution containing 20-40% caustic soda is added as the mixture is heated to its boiling point.

After the unreacted ECH evaporates, the resulting mixture is separated into two phases by introducing an inert solvent like Methyl isobutyl ketone (MIBK). Subsequently, the resin is washed with water, and the solvent is removed through vacuum distillation.

Producers incorporate certain additives tailored to the intended application to impart specific properties such as flexibility, viscosity, colour, adhesiveness, and faster curing to the resin.

To transform epoxy resins into a hard, infusible, and rigid material, they must be cured with a hardener. The curing process can occur at a wide range of temperatures, typically between 5 and 150 degrees Celsius, depending on the choice of curing agent. Primary and secondary amines are commonly utilised as curing agents for epoxy resins.

How is it used

Epoxy resins are incredibly versatile and find extensive use across many industries.

- In the adhesive industry, epoxy resins provide exceptional bonding properties, making them indispensable for various applications.

- They also play a crucial role in the coatings industry, where epoxy-based coatings offer superior protection, durability, and corrosion resistance, meeting the stringent requirements of sectors such as automotive, aerospace, and construction.

- In the electronics sector, epoxy resins are employed for encapsulating electronic components, circuit boards, and insulating materials.

- Within the construction field, epoxy resins are utilised for flooring, waterproofing, and concrete repair due to their remarkable strength and chemical resistance.

The aerospace industry uses epoxy resin in many innovative ways, including spacecraft hardware fabrication, space suit reinforcement, and improving flame retardancy. This thermosetting polymer’s combined adaptivity and flexibility make it ideal for use in many space travel solutions. They are also used in spacecraft for staking, sealing, coating, encapsulating, potting, and bonding various structural, electronic, and mechanical components.

They also play a vital role in water resistance and structural integrity in the marine industry. At the same time, the automotive and aerospace sectors rely on them for lightweight composites, adhesives, and coatings that enhance performance and safety.

These are just a few examples of how it contribute to various industries, showcasing their versatility and exceptional properties.

How can Redox help

Redox sells and stores epoxy resin products in various countries, including Australia, the United States, New Zealand, and Malaysia.

Discover how Redox can empower your organisation and unlock the full potential of your sourcing capabilities. Contact us now and experience the advantage that Redox brings.

Redox are proud distributors of a range of products from United Initiators including CAROAT®.

CAROAT® is the preferred option to solve problems which are caused by super chlorination when using common pool & spa sanitizers, such as chlorine, bromine and other non-halogenated alternatives.

CAROAT® is characterized by the following:

- odourless

- fast dissolving

- a powerful oxidizer (high oxidation potential)

- oxygen-based, doesn’t contain chlorine

- unaffected by UV degradation

- compatible with sanitizers based on chlorine, bromine and other non-halogen based alternatives

CAROAT® is a non-chlorine oxidizer used for shock treatment applications. It has all the positive functionality of a chlorine oxidizer while avoiding the negative side effects.

CAROAT® is the preferred option to solve problems which are caused by super chlorination when using common pool & spa sanitizers

Download the United Initiators Pool & Spa technical bulletin here and if you have any questions you may refer them to our dedicated Watercare Technical Manager.

This versatile material can also be used in a range of other applications such as –

Denture cleaners: Effective main ingredient in cleaning tablets for dentures.

- Bleaching agent: CAROAT® has a bleaching effect comparable to that of organic peracids; in the TAED/perborate system it is particularly effective at low temperatures.

- Biocidal effect: Suitable as an additive to acidic cleaning agents with bleaching and disinfectant effect.

- Effluent treatment: Oxidative treatment of problematic effluents; sulfide oxidation, nitrite oxidation and cyanide detoxification.

- Plaster additive: Addition of CAROAT® leads to generation of oxygen and improved product characteristics (e.g. thermal insulation, water absorbency, mechanical properties).

- Metal treatment: Microetchant: Use for etching printed circuit boards.

- Textile finishing (shrink proofing of wool)

- Chemical synthesis (production of dioxirane)

- Paper manufacture (repulping, particularly of wet-strength paper).

About United Initiators

United Initiators is a global and leading producer of peroxide-based initiators, Hydrogen Peroxide and specialty chemicals. The company offers a broad range of organic peroxides, persulfates, Hydrogen Peroxide and selected specialty chemicals. Organic peroxides are used in a large variety of polymerization processes and polymer processing applications.

The use of persulfates ranges from aqueous polymerization processes, over electronics, disinfection, cosmetics, metal etching, paper treatment, Oil & Gas exploration to a broad field of bleaching processes. Hydrogen Peroxide is used in consumer goods, disinfection applications and is an enable for the world’s digital economy.

United initiators has several production facilities in Europe, North America, Asia-Pacific, Turkey and India. UI’s mission is to be the best serving peroxide producer for a growing world.

How Can Redox Help?

With Redox, rest assured that our unwavering commitment to excellence will empower your business.

Contact us today to discover how we can be an essential partner in your sourcing strategy, or click here to view the product page.

ICIS Chemical Business Magazine has released their annual Top 100 Chemical Distributors for 2023 and Redox has been ranked as the largest Australian distributor, 12th largest in APAC and the 34th globally.

This list includes 340 of the world’s leading chemical distributors with rankings based upon revenue achieved during Calendar Year 2022.

Of note Redox has climbed 30 places in North America as the company grows it’s presence in the US and Mexican markets, with new locations opened recently in Houston, Dallas and Seattle.

This result is an endorsement of the value that Redox has been able to deliver for clients and our suppliers through the good work of our dedicated team.

Click here to read the full report.

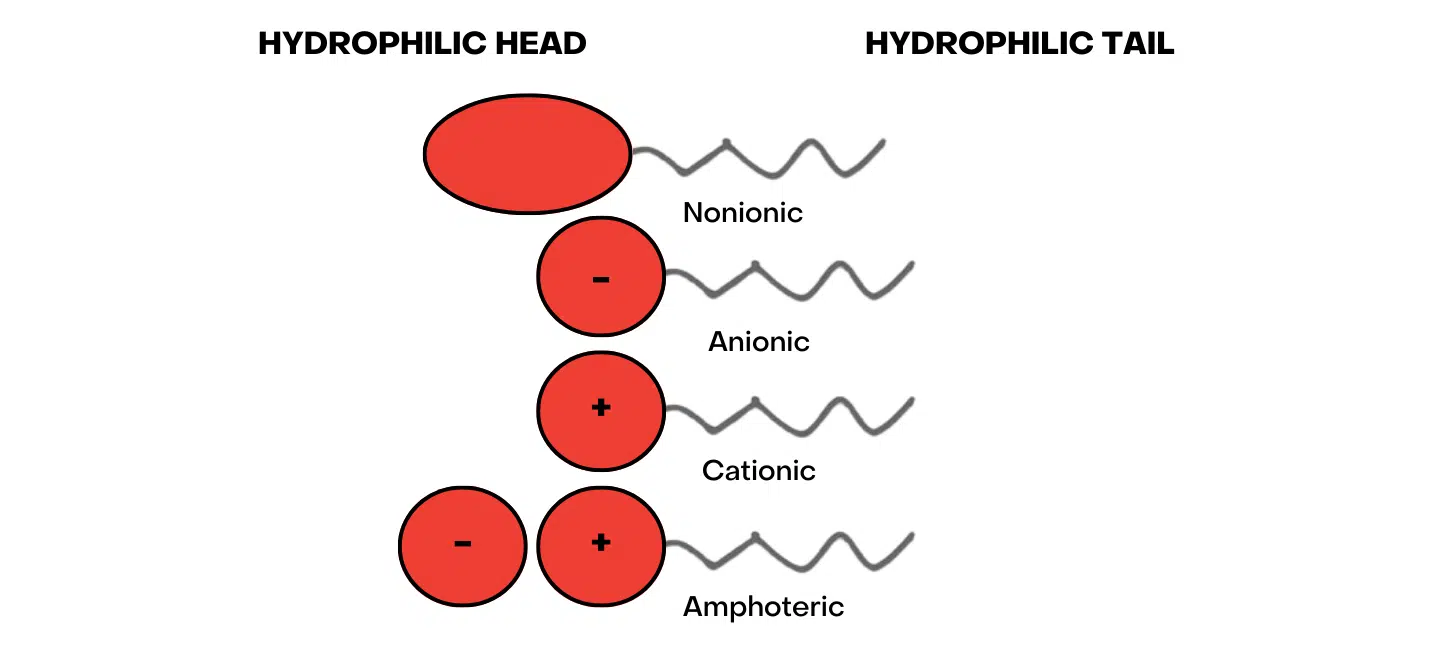

A surfactant, also known as a surface-active agent, is a substance that lowers the surface tension between two substances. It is a molecule that contains both hydrophilic (water-loving) and hydrophobic (water-hating) parts, allowing it to interact with water and oil.

Surfactants are a wide spectrum of products but are broadly classified as Anionic, Nonionic, Cationic or Amphoteric depending on whether the electrical charge is positive, negative or neutral on the hydrophilic head.

Surfactants are commonly used in cleaning products such as detergents, soaps, and shampoos. They can break down oils and dirt and help them mix with water for easier removal. They are also used in industrial processes such as oil recovery and in medical applications such as lung surfactants, which help maintain the structure of the lungs and prevent collapse.

Examples of surfactants include sodium lauryl sulphate, commonly found in household cleaning products and personal care items, and polysorbate 80, used in food, cosmetics, and pharmaceuticals.

Surfactants are used in a wide variety of products, including:

- Detergents and cleaning products: Laundry detergents, dishwashing liquids, all-purpose cleaners, and bathroom cleaners all contain surfactants that help to remove dirt, oil, and grease from surfaces.

- Personal care products: Shampoos, body washes, hand soaps, and toothpaste all contain surfactants that help to clean and remove oils from the skin and hair.

- Cosmetics: Makeup removers, facial cleansers, and body wash contain surfactants that help break down and remove makeup and other impurities.

- Food and beverages: Emulsifiers and stabilizers are surfactants used in food and beverage products to help mix ingredients that would not usually mix well, such as oil and water.

- Agriculture: Surfactants are used in agricultural products, such as herbicides and pesticides, to help them stick to plants and improve their effectiveness.

- Petroleum: Surfactants are used in the petroleum industry to improve oil and gas flow through pipelines and help recover oil from underground reservoirs.

- Lubricants: By adding surfactants to car engine lubricants, it becomes possible to prevent particles from adhering to engine parts, enabling the parts to move smoothly and maintain the proper functioning of the car.

Surfactants have several unique qualities that make them useful in a wide range of applications:

- Surface tension reduction: Surfactants have the ability to reduce the surface tension between two substances, such as water and oil. This allows the substances to mix more easily and enhances the ability of the surfactant to clean, emulsify, or disperse.

- Amphiphilic nature: This unique structure allows surfactants to interact with water and oil hydrophilic (water-loving) and hydrophobic (water-hating), essential for their cleaning use and emulsifying.

- Self-assembly: Surfactants can self-assemble into organized structures, such as micelles or bilayers, in certain conditions. This allows them to form stable emulsions, which are essential in creating many products such as lotions, creams, and paints.

- Interfacial activity: Surfactants are active at interfaces, such as the boundary between two liquids or a liquid and a solid. They can adsorb to the surface of a substance, which can change its surface properties, such as its wetting or adhesion behaviour.

Overall, these unique properties make surfactants extraordinarily versatile and valuable in a wide range of applications, from cleaning products and personal care items to industrial processes and medical applications.

Did you know that Hydrochloric Acid is also known as HCL, muriatic acid, or spirits of salt? It’s utilised in a variety of industrial and commercial settings. For those who work in industries that use this chemical, it’s vital to understand the most common applications, what they accomplish, and what you need to know to handle them safely and responsibly.

What Is Hydrochloric Acid?

Hydrochloric Acid is an odourless, colourless solution of hydrogen chloride in water with a pungent smell. But behind this almost invisible veneer lies a powerful punch. For instance, Hydrochloric Acid can react with metals to form an explosive gas. Yet, it can also be found in many home cleaning products.

1150 kg IBCs housed in our warehouse, classified Hazard Class 8, are for corrosive materials, defined as substances that can cause significant harm to living tissue and/or corrode steel and aluminium if they leak.

Hydrochloric Acid is classified as a class 8 hazardous product, i.e. it’s a corrosive substance and can cause burns and irritation to the skin. Due to its corrosive properties, extreme care must be taken when handling this product. Make sure to wear appropriate safety equipment when handling hydrochloric acid. Ensure to avoid direct eye contact; if this occurs, seek immediate medical advice.

We recommend you consult the safety data sheet when using, storing or handling the product.

Hydrochloric Acid in the market and its many uses

This potent acid is found in many industries and has a wide range of uses.

What is Hydrochloric Acid used for?

The most significant end uses for Hydrochloric Acid are cleaning, the productions of fertilisers and dyes, steel pickling, oil well acidising, food manufacturing, producing calcium chloride, and ore processing.

How it’s used also varies significantly. For instance, in water treatment, it’s used to control pH levels, or in swimming pools, it can help remove any stubborn algae from the floors and walls of your pool. In acidising oil wells, it helps remove carbonate reservoirs, or limestones and dolomites, from the rock. It’s used in laboratories for acid-base titrations and for producing organic and inorganic compounds like PVC.

We also find substantial use of Hydrochloric Acid across many other industries like:

- Mining,

- water treatment,

- oil/gas,

- detergents,

- leather, building,

- textile,

- rubber,

- photography.

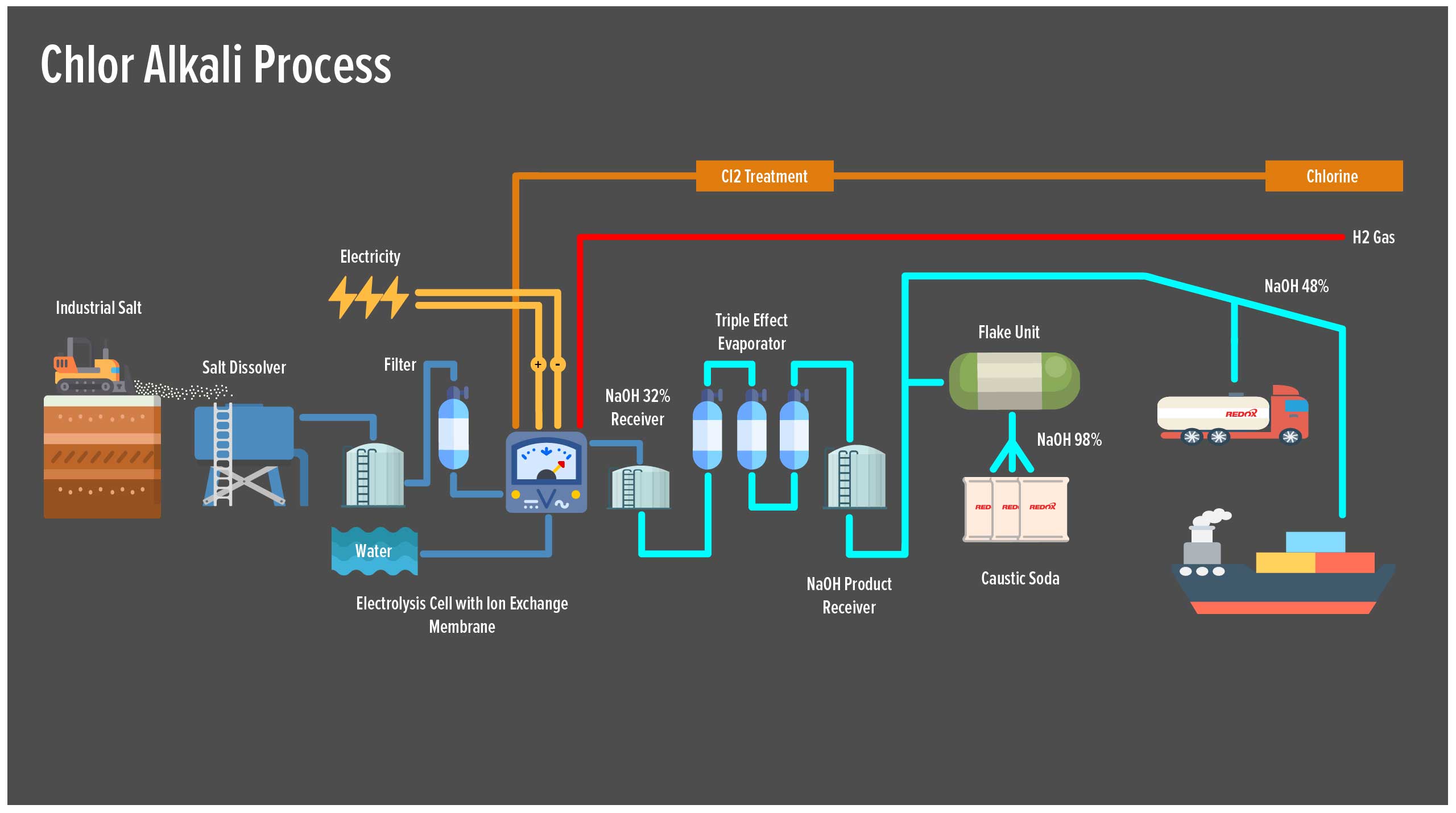

Hydrochloric acid is manufactured predominantly in industrial chlor-alkali plants around the world. The process involves the electrolysis of sodium chloride (salt) solution . This produces chlorine gas , sodium hydroxide and hydrogen gas. The hydrogen is then used to produce hydrochloric acid and ammonia.

In 2020 the global Hydrochloric Acid market size was US $7.8 billion and was expected to record a revenue CAGR of 1.5% over the forecast period through 2028.

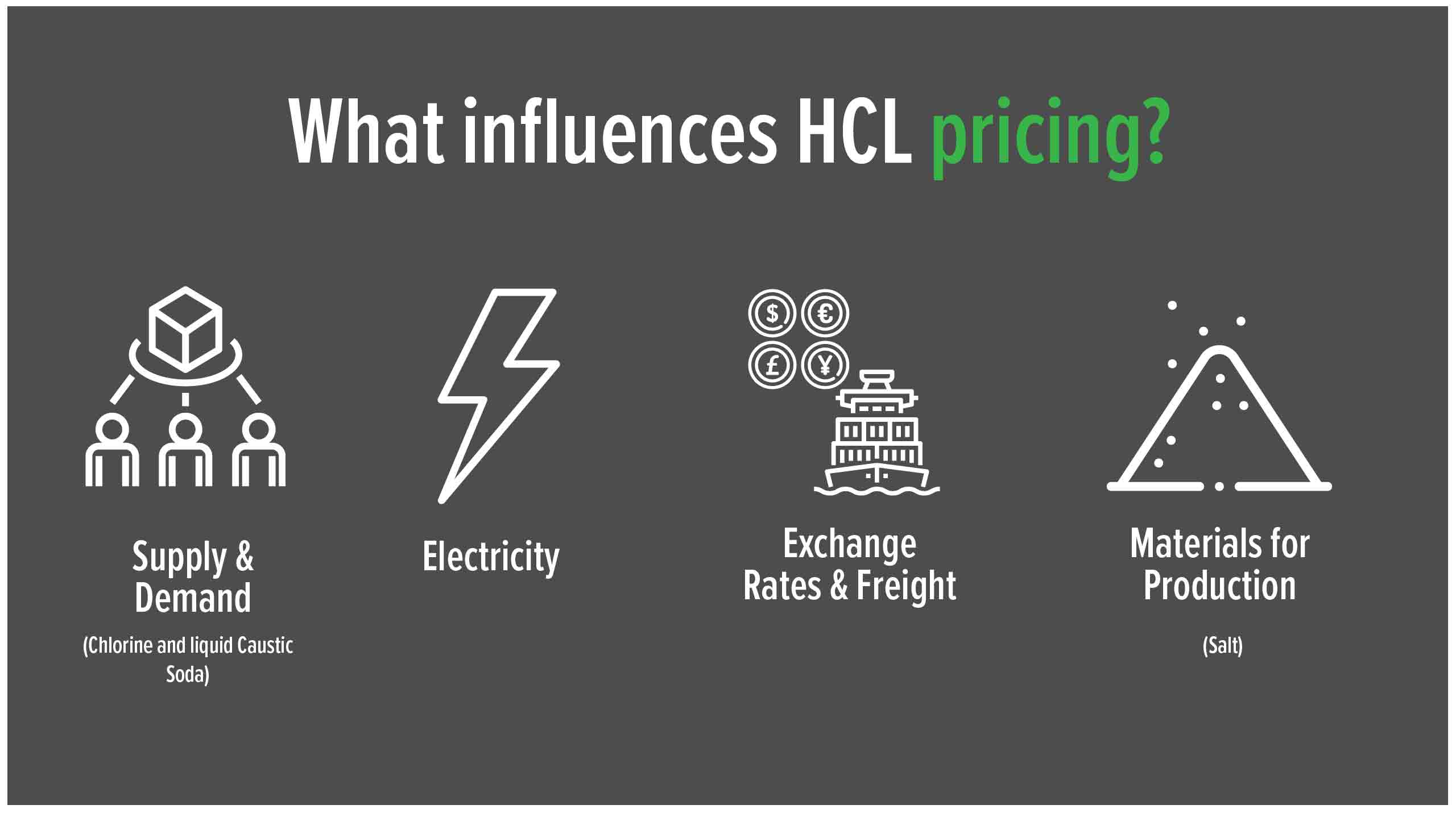

HCL prices are usually fairly stable and tend to increase yearly as a result of CPI increases, usually as a result of the cost of production (labour /electricity costs etc). However, the imported cost of the product is highly dependent on exchange rate variations, packaging and sea freight costs. Finally the overall economics of supply and demand would also play a role in the change in the price of HCL, which is also dependent on Chlorine and liquid Caustic Soda demand, which are all part of the chlo-alkali process.

Hydrochloric Acid In The Home

In the home, you’re most likely to find it used in cleaning agents like toilet and tile cleaners, as it removes grime without reacting to many bathroom surfaces.

Is Hydrochloric Acid Corrosive?

In short, yes. Hydrochloric Acid is corrosive to organic tissues and will corrode mucous membranes, eyes, skin. It can also be corrosive to almost all metals.

How can we help you?

Redox’s Hydrochloric Acid is available in various pack sizes, including 20-litre carboys, 240 kg drums, 1150 kg IBCs and bulk tanker/Isotainers loads. The product comes in a range of strengths ranging from 6% to 33%, with 32% hydrochloric acid being the main commonly used strength.

Contact one of our experts to discover how Redox can be essential to your sourcing strategy.

Lactic Acid is a versatile material found in a variety of innovative products that was first discovered by the Swedish chemist Carl Wilhelm Scheele in 1780 and produced commercially by Charles E. Avery in 1881.

It’s Applications in Industry?

Lactic Acid is a naturally occurring organic acid utilised in various industries, such as cosmetics, pharmaceuticals, chemicals, food, and, most recently, medical industries.

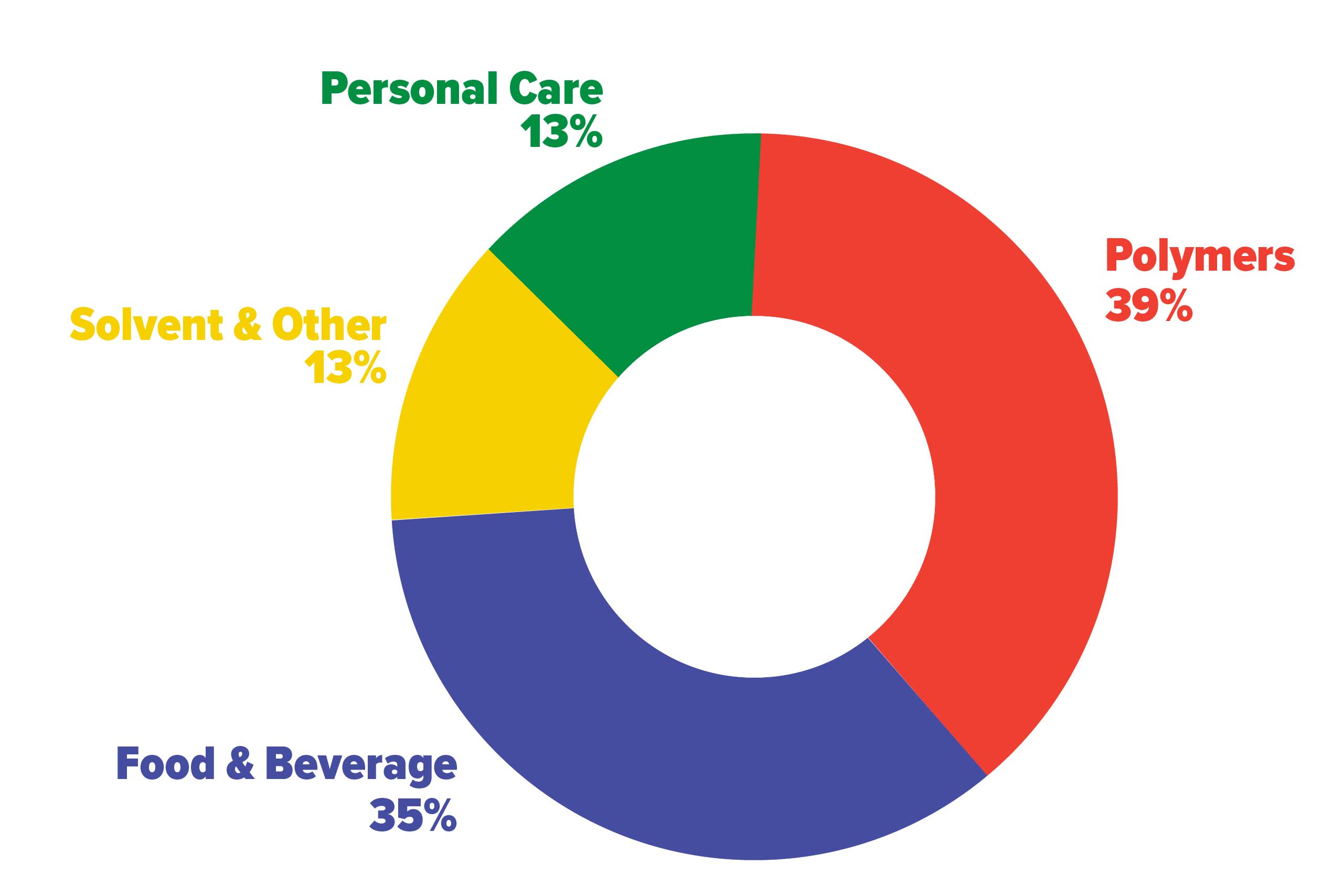

In the food industry, which accounts for a large portion of the demand (35%), it has several uses:

- It acts as an acidifier for bread,

- prevents the development of harmful bacteria in pickles, relishes, salad dressings,

- adds a mild-tasting sourness to beverages and candy,

- In dairy products, it is used to prevent fermentation and,

- It is an essential ingredient in fermented foods, like yoghurt, butter, and canned vegetables.

However, it is also used as an antimicrobial in cleaning products, has applications in the leather tanning industry, in descaling processes, in the textile industry as a mordant (fixative) for dyeing, and can be converted to ethanol, propylene glycol, and acrylic polymers in the chemical industry.

Fig. 1. Uses and demand of lactic acid (The Essential Chemical Industry Online 2013)

Although it’s been commercially available for a long time, it is only in recent decades that new uses have resulted in a tremendous increase in demand.

For example, its an essential building block in producing a range of new and innovative bioplastics, PLA or Polylactic Acid – the new generation of biodegradable polymers.

The use of Lactic Acid in manufacturing environmentally friendly, green solvents is another area for significant potential growth. Using it as a green solvent enriches the diversity and versatility of bio-based green solvents and could offer an effective means for designing environmentally benign synthetic systems.

Its application and innovative usefulness seem ever-growing, and in 2010, it was included in a report issued by the U.S. Department of Energy on chemicals that are considered potential building blocks for the future.

Lactic Acid from Redox

Redox is proud to work with leading manufacturers of Lactic Acid and Lactates globally and can create solutions for all customer requirements.

Redox supplies Lactic Acid in the Australian, New Zealand, Malaysian, and North American markets and is available in various packing sizes. These include 25kg carboys, 250kg steel drums and 1200kg IBCs.

We offer it in a range of varied strengths, with a powder form also available for specific applications. Our Lactic Acid conforms to the Food Chemicals Codex (FCC), ensuring our product’s overall safety and integrity.

Contact one of our experts to discover how Redox can be an essential element of your sourcing strategy.

Our Partnering Manufacturers